Navigating Long-Term Care Insurance

You may know long term care as elderly but it’s the same care: it’s care when you need help caring for yourself. That usually occurs later in life.

The definition of whether someone qualifies for non-taxable long term care benefits is defined in US law as either physical or cognitive impairment.

Physical

There are six “activities of daily living”, in no particular order;

- Eating

- Bathing

- Dressing

- Transferring (such as in/out of bed)

- Toileting

- Continence (control of bowels and bladder)

Under many long term care insurance policies, if you cannot do any 2 of 6 of the above physical activities of daily living without help, you qualify as having a long term care condition.

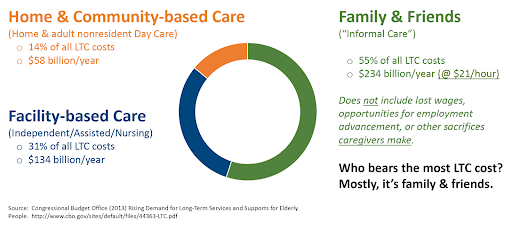

If you don’t have long term care insurance (most Americans do not), you might rely on family to care for you. Family provides the most care in the US.

A cognitive impairment alone (dementia, Atzheimer’s, Parkinson’s, other conditions) may qualify you for long term care benefits.

A long term care condition, by definition, is expected to last at least 90 days. That generally distinguishes long term care from a condition from which you are expected to recover.

Medicare does not pay for long term care.

Medicaid may pay for nursing home care but this type of care is only used by 4.5% of Americans at any given time, is usually among the last types of care needed (not the first), you generally need to spend down your own assets to qualify, and you do not necessarily get your choice of facility.

Most Prefer Care In Their Home

When people think of long term care one of the first things which come to mind are the words “nursing home”. Most people prefer to receive care in their own home.

Types of Facility

Cost depends on the level of care (independent, assisted, skilled nursing, other types) and, like hotels and star ratings, cost is based on many factors. The higher the level of care needed, the higher the cost. You can generally find a range of options reflective of the quality of the facility, staff, and reviews.

Care Like a Staircase

Generally, when one needs long term care it’s for a few hours per day and a common age to begin this care is around age 85. As one ages, additional hours of care may be added because additional care supervision is needed. The need to be in a facility, independent living, assisted living, or a skilled nursing facility (aka a “nursing home”) is generally because the individual needs the always-available supervision and amenities these varying levels of care provide.

Cost and the Baby Boom Generation Impact

The cost of long term care is one of the biggest threats to your financial well-being in retirement because the cost is in addition to your normal costs. As has been the experience of the Baby Boom generation, this demographic group changes the dynamics by its sheer numbers. Long term care may be no different. As Baby Boomers demand long term care services at the same time, expect the cost of everything related to long term care to rise. That makes it that much more important to plan how to manage these costs.

Some Cost Estimates

Direct hire home health aide: $14-16 per hour

You are responsible for recruiting/hiring/firing and making sure there is a caregiver whenever you need it. One of the most challenging aspects of the caregiving industry is finding and retaining good caregivers.

Hire an Agency: $21-$26 per hour

You hire the agency and the agency takes care of everything else.

Food for Thought

If you’re reading this, you’re likely either in your 50s or 60s and looking for information to help care for a parent or elderly relative. But, you may very well be in the same position some day they are in today.

One of the great tests of human nature is how we treat other people. Setting an example for your children to follow in how to care for parents may be one of the most important examples you can set. You’re setting an example for the care you may want someday, too.