Early Career Investment

There’s a reason everyone’s heard of “Wall Street”. Much that has to do with money and investing has and still does originate from the industry called “Wall Street”–even if many of the investment firms we associate with “Wall Street” are not necessarily based on that street in New York City.

Getting a Little Wall Street In You

Wherever you are, you’ll probably be an investor so you should know a little about investing to help you make informed financial consumer decisions about your money.

As someone in the early years of your career, you may have many questions about investing. After all, you might not have ever taken a course in investing, had an interest in investing, or read about it. But it’s important to know some investing basics.

Financial Goals

We all have goals and, often, we need money to reach those goals, such as:

- Working because you want to, not because you have to

- Funding your children’s college education (or any level of education)

- Starting your own business

- Minimizing/Reducing debt

- Saving for a house

- Building wealth

Whatever your financial goal, investing is the way you’re likely trying to achieve it.

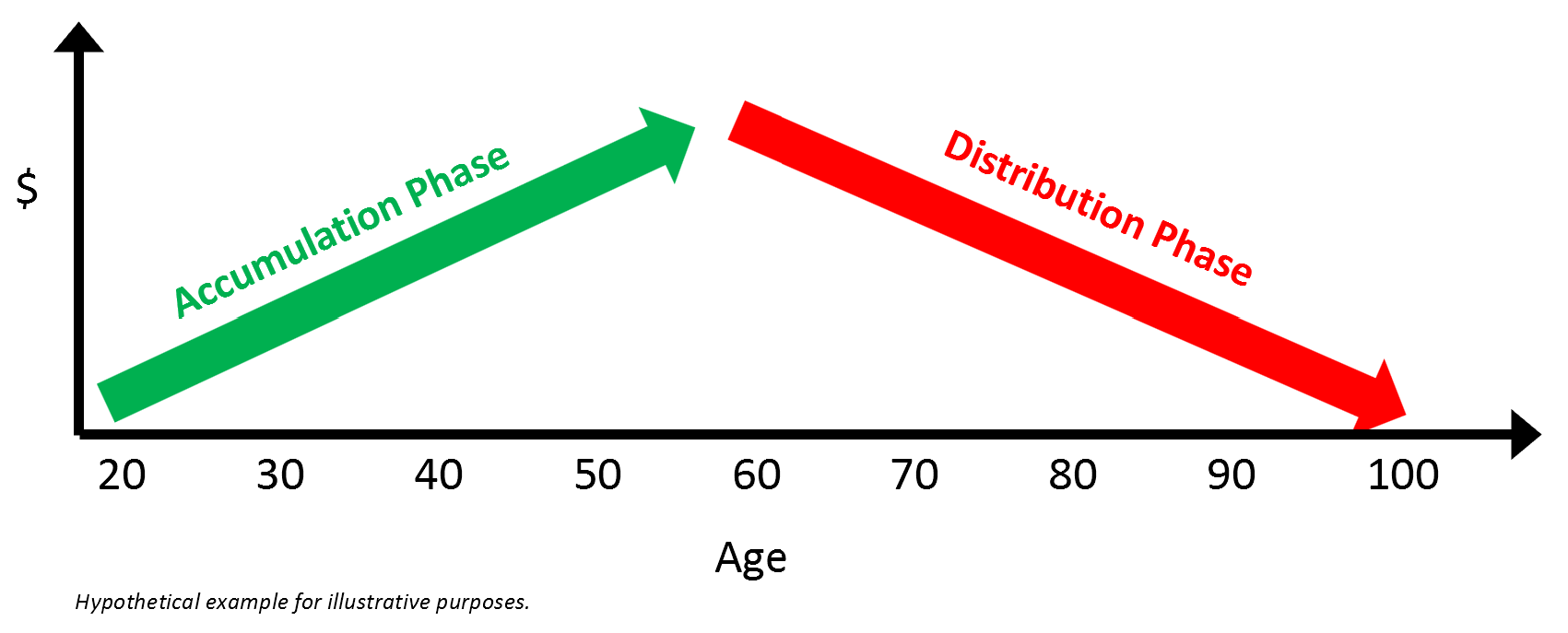

Two Phases: Accumulation and Distribution

Let’s take retirement as an example. The money you invest will likely come from your paycheck. You may deduct a percentage of each paycheck toward your retirement account. That money will (likely) be spread across many different investment options you chose (generally and indirectly) based on your tolerance for investment risk (when you sign up for your employer’s or any investment plan you’ll be asked some investment behavior questions which will determine your general investment risk tolerance, anywhere from conservative to moderate to aggressive). This is the accumulation phase of investing. You are accumulating money for use at a later time, namely to take later as retirement income.

Contribute More Than The Match

The distribution phase begins when you start taking (distributing) money from your retirement account. You may have stopped working–by choice or not. Now you need to use the retirement money you’ve saved as income.

Will you have enough to maintain your purchasing power (against inflation) to last as long as you do? That’s the big question you’ll face later in life. The older you is counting on you today to save enough for tomorrow! Remember, it’s income that’s the goal, not the investing road to get to the goal.

How much do you need to save to reach your goals? Use this calculator to find out.

Find an Advisor

Financial Terms You’ll Encounter

Roth

Anything with a “Roth” in its name is an after-tax investment account. That means you’ll pay income tax before you invest. Money you distribute for use as income later will not only not be subject to income tax (because you already paid it) but you will not report this income on your tax return when you take it from your account (because you did that, too, when you paid tax on it years earlier).

401k | 403b | 457 | IRA | SIMPLE | SEP

There’s an alphabet soup of retirement plans that are recognized by the IRS. Depending upon the type of employer you have, you may participate in one of these plans.

These are all names of retirement accounts, often based on the section of the tax code in which they appear. They are all pretax accounts, meaning the money you invest has not been taxed (but you generally may take a deduction from your income on your tax return in the year you invested this money which may reduce your taxable income that year). When you take the money from this account you’ll pay income tax on it.

You Have Options

You have options when it comes to your money. The more informed you are about financial options the more informed of a financial consumer you are likely to be.

Take Our Quick Financial Quiz

How financially literate are you compared to the average American? You can take one of the shortest of those financial literacy quizzes here (it’s only 6 questions) to get a taste of the questions asked.

Take Our Quiz