There are numerous ways to use, invest, and save your money. What you need is a framework to help you understand what you’re doing and why. Having a sensible, easy-to-understand framework can help.

The following Financial Priorities Pyramid may provide the foundational vision you need, especially those who are just starting out in the workforce and may be searching for a better understanding of money and how it fits into your life.

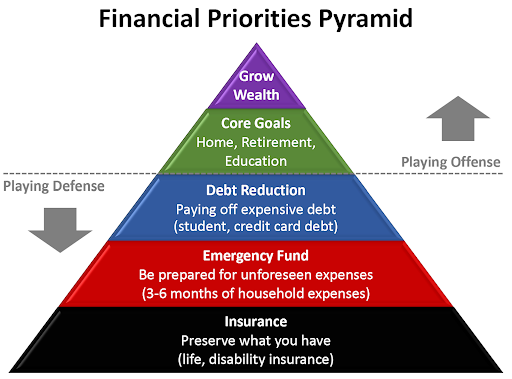

Build from the ground up, starting with the black foundation layer (Insurance). Before you can build wealth (the top of the pyramid) you need to manage your risks, if you’re exposed to that risk. Apply these priorities to your monthly budget–how you spend your money.

Insurance

If you have someone (a spouse, children, a pet) who is financially dependent on you, you have a responsibility to provide for them. They are counting on you. For risks beyond your control, you might consider buying insurance to financially protect those dependents when you cannot.

If you don’t have such responsibilities or don’t have them yet, you can skip this level and focus on the next level (Emergency Fund).

Emergency Fund

Let’s face it, an unforeseen large expense, such as a medical bill, a roof to fix, pet surgery, you lost a job and are without a paycheck, you’re temporarily disabled and without a paycheck, have a major car repair, or some other expense can occur at the worst possible time. An expense like this can throw your cash flow into a long term tailspin if you’re not prepared.

It’s not a financial emergency if you have an emergency (or “rainy day”) fund, generally equal to 3-6 months of household expenses saved up. That fund can buy you time and help absorb these financial shocks.

Debt Reduction

The next level of the pyramid priority list is about debt reduction. We’re talking about high cost debt from a credit card, student debt, or other debt that’s usually not secured by an asset (like a home). High cost debt is a burden on your monthly cash flow and poses a risk because creditors have a claim on your financial resources and well-being. You don’t want that.

There are generally two strategies to get yourself out of debt. Choose one.

- The “Snowball” strategy suggests you focus on your smallest debt and pay that off first to build achievement momentum. Then, target the new smallest debt you owe and start paying that off and so on.

- The other strategy suggests you target your highest interest (cost) debt. You should pay that off first because it’s costing you the most.

Paying off high cost debt can help free monthly cash and improve your credit score. The goal is to change from being a debtor with liabilities to being an owner of assets: from debt being a burden on your budget to your having budgeting power.

Financial Goals

We’re talking about core personal financial goals to you and your family, such as saving/investing to buy a home, contributing to your retirement account, or to fund your child’s education. These are financial goals that have a meaningful impact on your life and those you care about most. They take time to pursue but they are about buying equity in assets, investing in the people you love, and creating financial security you control.

At this point, look at your financial position and be able to see the following:

- You’re using insurance to manage risks you cannot control.

- You have an emergency fund that helps to prevent financial stress because you’re confident you can handle an unforeseen expense.

- You have control over your household monthly budget (cash flow). You’re meeting your needs and have a surplus at the end of each month. You’ve built credit by having a high credit score, you have credit extended to you via credit cards, car loans, etc. and have built equity in your home, if you’re a homeowner.

- You’re pursuing (and tracking) financial progress through retirement accounts, equity in your home, and control over your financial affairs. Your goal is to have the resources to be able to work because you want to, not because you have to.

Grow Wealth

It may seem like this step would take a long time to reach but if you’re careful with your money, you’re likely to encounter the opportunity to work on this top level of the pyramid sooner than you think.

With the other foundational layers of your financial pyramid addressed, you may be in a very good financial position to pursue projects that have the potential to provide you with substantial discretionary income and assets, such as starting a new business, investing in real estate, and expanding your investments beyond your needs.

That’s the vision. A strong financial foundation pyramid can help provide a lifetime of financial support.