Debt Management

When we think of investing we think of returns. How much return does an investment offer in exchange for a certain amount of risk?

The Opposite of Investment Return

There’s an opposite side of return on your investment. It’s the interest rate charged on debt you owe. What’s charged to you as an interest rate is a return to the company that loaned you that money. It’s a return to them at your expense.

The not-so-funny thing is that unlike an unknown return on your investment–because you have to wait to see how that investment performs–the interest rate charged on your loan is often fixed. There’s no uncertainty about how much you’ll pay. Rather, the risk to the creditor is whether you’ll pay (credit risk).

Good and Bad Debt

Debt isn’t necessarily a bad thing. Debt has helped to build both America and Americans. When debt is used to help enable an improvement–to develop land, a factory, a farm, a person–it can be helpful. But when debt is used simply as a means of spending beyond your means, the debt burden can be debilitating. That’s why it’s important to have a basic understanding of how to manage debt.

Debt Management

On the one hand, when you’re young you have lots of time ahead of you for investment growth to compound. You want that.

On the other hand, when you’re young you usually haven’t yet had the time to establish a strong credit score and corresponding credit history. Without that–such as when you were “rewarded” with student financial aid–the interest rate you were charged was higher than it might have been. You don’t want that.

How to reconcile these two in terms of debt management? Generally, if the interest rate you pay on debt is higher than the return you confidently (adjusted for risk) get from an investment, then you should consider paying off your debt first. This is one reason mortgages are paid over so many years: because they are backed by real estate and qualified borrowers and, as a result, have a correspondingly low interest rate that can be exceeded typically by higher return investments.

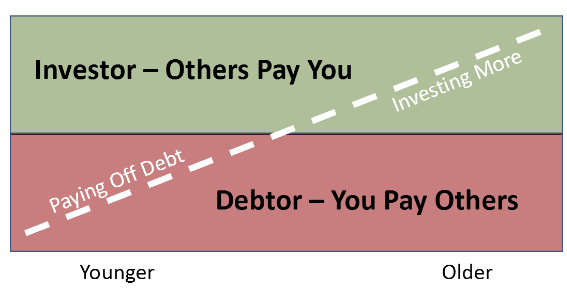

Your experience using your available funds to first pay off debt then use the freed up surplus to invest more may look something like this diagram.

Credit card and student debt pose a similar debt management problem. Each generally has higher interest rates and should be paid off before investing. This is especially true if your debt is variable–changes when interest rates change. If interest rates rise, the cost of your debt may rise and that can place a larger burden on your monthly budget.

Compound Interest

Compound interest is one of the strongest characteristics of finance. It can hurt or help you.

If you had $100 and earned a 10% return this year, you’d have $110 at the end of the year. If you earned another 10%, you’d have $121, not $120, because this year’s 10% growth would be on the $110, not the original $100 (that would be called “simple” interest).

When you’re investing, compound interest can help you. When you’re in debt and have difficulty paying that debt, your interest rate costs can compound against you. Those forces can get stronger with rates and time so it’s important to keep them in check–or pay them off–so they don’t become a larger, debt snowballing problem.